PayPal's AI Lifeline: Deconstructing the Hype Behind a 15% Surge

The market loves a good story, and on Tuesday, it got a great one. PayPal (PYPL) shares rocketed up nearly 15% in premarket trading on the heels of a blockbuster announcement: a partnership with OpenAI to embed its digital wallet directly into ChatGPT. The narrative is clean, powerful, and perfectly timed for an era obsessed with artificial intelligence. The logic seems simple: connect PayPal’s 400 million users with the “hundreds of millions” flocking to ChatGPT, and you’ve created a commerce superhighway.

On the surface, the numbers released alongside the announcement seem to validate the euphoria. Headlines declared that PYPL Stock Rises After Company Raises Annual Profit Forecast, Plans To Embed Digital Wallet In ChatGPT, and the details seemed to back it up. The company raised its annual adjusted earnings per share (EPS) forecast, now expecting between $5.35 and $5.39. Its third-quarter results handily beat Wall Street estimates, with revenue hitting $8.4 billion against an expected $8.23 billion. CEO Alex Chriss painted a picture of seamless synergy, where users can “go from chat to checkout in just a few taps.” Retail sentiment, as measured by chatter on platforms like Stocktwits, flipped from ‘bearish’ to ‘extremely bullish’ almost overnight.

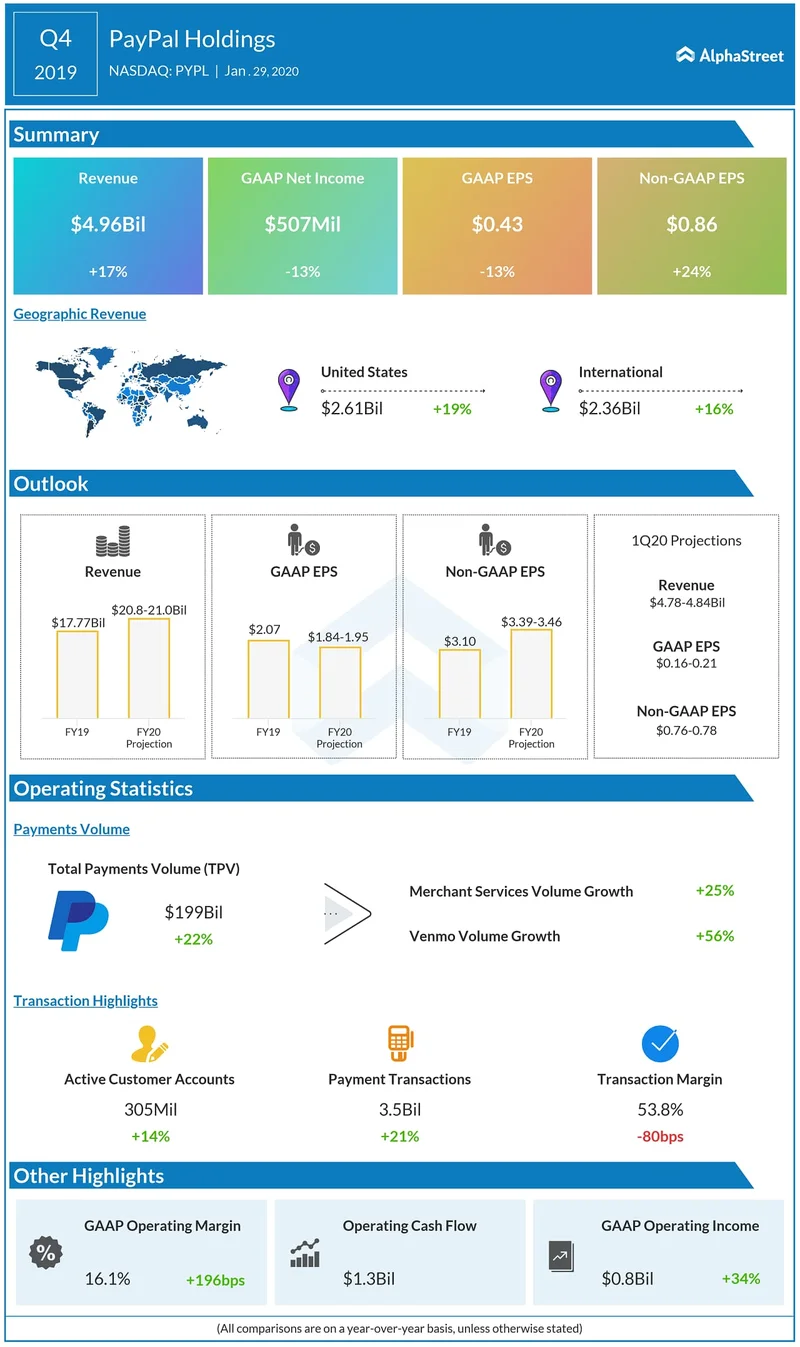

It’s a compelling package. So compelling, in fact, that it almost makes you forget to look at the other numbers. The ones that don’t fit the story quite so neatly. While the market was busy celebrating the future of AI-driven commerce, I was looking at a single, deeply troubling data point buried in PayPal’s own Q3 report: a 5% year-over-year decrease in total payment transactions.

For a company whose entire business model is predicated on facilitating transactions, a decline in that core metric is a flashing red light on the dashboard. It suggests a potential erosion in usage or market share. This isn't just a minor blip; it's a direct contradiction to the growth narrative being sold.

The Art of Selective Data

PayPal, of course, has an explanation. The company was quick to add a crucial qualifier: "Excluding payment service provider transactions, payment transactions increased 7%." This is a classic piece of corporate messaging. It reframes the data by carving out a specific, undefined segment to produce a positive number. The immediate, and most important, question is one of methodology: what exactly constitutes these "payment service provider transactions," and why is their decline so significant that it drags the entire metric into negative territory? We aren't given the details.

And this is the part of the report that I find genuinely puzzling. I've analyzed hundreds of these earnings releases, and this type of selective data presentation is almost always a strategic choice. It’s designed to direct your attention away from a problem area. The OpenAI partnership, announced with such fanfare on the very same day, feels less like a coincidence and more like a beautifully executed piece of narrative management. It’s the shiny object meant to distract from the fundamental health of the core business. Is this new venture a genuine engine for future growth, or is it just a fresh coat of paint on a house that might have some foundational issues?

Let’s be clear. The stock was down significantly for the year before this news—to be more exact, it had fallen nearly 18% year-to-date. This 15% jump, while impressive, is primarily recovery, not new value creation. It’s a return to form fueled by a story about tomorrow, not a reflection of the business today. The partnership itself is built on a protocol (the Agentic Commerce Protocol, or ACP) with a rollout planned for 2026 for product catalogs. That’s a long time to wait for a tangible impact. How much revenue will this generate in the next fiscal year? What percentage of ChatGPT users will actually convert to buyers via PayPal? These are the questions that matter, and the answers are pure speculation at this point.

The OpenAI deal is like a high-stakes bet on a promising but unproven technology. It’s a lottery ticket purchased with investor enthusiasm. It could pay off spectacularly, creating an entirely new commerce channel. Or, it could fizzle out, becoming another forgotten integration in a long line of tech partnerships that sounded better in a press release than they worked in practice. Meanwhile, that 5% transaction decline remains a present-day reality.

A Calculated Distraction

Let’s call this what it is: a brilliant strategic move to change the conversation. The market wasn’t buying PayPal’s turnaround story based on its existing business, so management went out and bought a new story—one with "AI" in the headline. The subsequent stock surge has nothing to do with a sudden improvement in PayPal's fundamentals and everything to do with sentiment and keyword association.

The raised guidance is certainly positive, but it can’t entirely mask the operational weakness suggested by the decline in transaction volume. That single metric is the most honest indicator of PayPal’s current health. Until the OpenAI partnership can demonstrate a material, measurable reversal of that trend, it remains an expensive and well-timed distraction. I don’t analyze press releases; I analyze balance sheets and cash flows. And right now, the story and the numbers are telling two very different tales.